Is It Worth Considering Development Loans or Bridging Finance as a Self-Employed Borrower?

If you’re self-employed — whether you run your own business, operate as a company director, or invest in property — you’ll probably already know that the standard mortgage route doesn’t always fit neatly around the way you work or the pace at which opportunities come up.

This is especially true when you’re buying at auction, funding a renovation, or trying to get a development project off the ground. In those situations, development loans and bridging finance tend to come into the conversation quickly.

One of the things we hear a lot is whether these kinds of finance are a realistic option for self-employed applicants — particularly when your income is already viewed a bit differently by lenders. There’s also a fair amount of uncertainty around the costs involved, the risks, and whether it’s the right tool for the job in the first place.

The honest answer is that both bridging finance and development loans have a genuine purpose when they’re used in the right way. The trick is understanding how they work and whether they make sense for what you’re trying to achieve.

Why self-employed borrowers look beyond standard mortgages

If you’ve already been through the process of applying for a mortgage as a self-employed person, you’ll know that lenders typically want to see one to two years of accounts, a consistent income, and clean financial records. That’s fine for a standard purchase — but certain opportunities simply don’t wait around for that kind of timeline.

Auction purchases are the obvious example. You’ve got a fixed completion deadline, and a traditional mortgage often just can’t move fast enough. The same applies to properties that are in poor condition and wouldn’t meet standard mortgage criteria, or investments where the window to act is tight.

That’s where bridging finance and development loans come into their own. They’re built around short-term or project-based funding rather than the long-term borrowing that a standard mortgage represents.

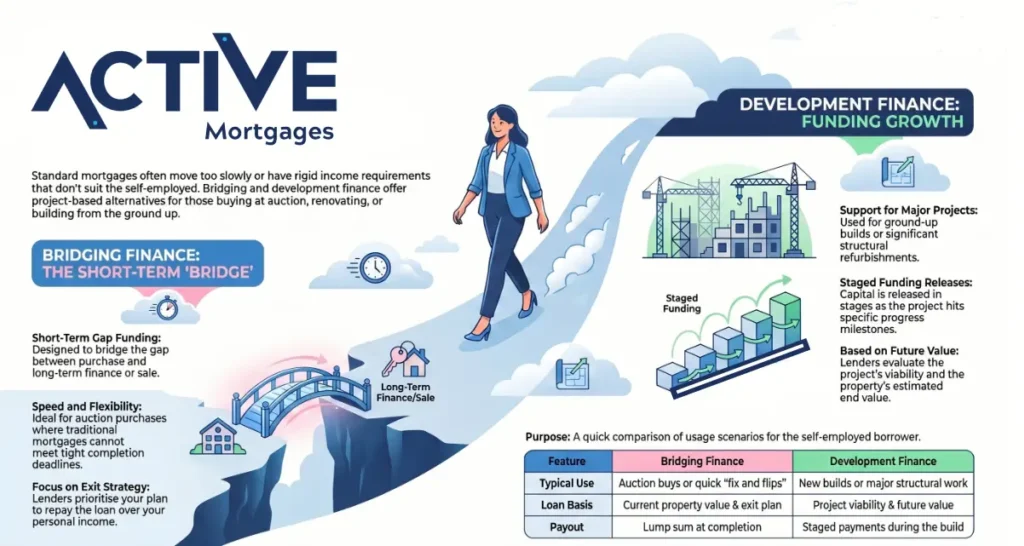

So, what is bridging finance?

A bridging loan is essentially a short-term loan designed to “bridge” the gap between buying a property and either arranging longer-term finance or selling something else.

A typical example would be using a bridging loan to buy a property that’s not currently in a state where a standard mortgage lender would touch it, doing the work needed to bring it up to scratch, and then refinancing onto a normal mortgage once it meets the right criteria.

Bridging loans tend to appeal to self-employed investors because they’re faster and more flexible than traditional mortgages. Lenders are often more focused on the property itself and your plan for getting out of the loan than they are on your income in isolation.

That said, it’s important to go in with your eyes open. Bridging finance is more expensive than a standard mortgage — the interest rates and fees are higher — so it really is best suited to short-term use where you’ve got a clear plan in place from day one.

And what about development finance?

Development finance is typically for bigger or more structured projects — building new properties from the ground up or carrying out significant refurbishments rather than a quick cosmetic spruce-up.

The funding is usually released in stages as the project progresses, rather than all at once. Lenders will look at how viable the project is, what experience you have as a developer, and what the property is expected to be worth once the work is complete.

For self-employed applicants — particularly those working through a limited company — development finance can be a practical way to fund projects that a high street lender simply wouldn’t consider. As with bridging, the lender’s focus will be on the strength of the project and your exit strategy, whether that’s selling the finished property or refinancing onto something longer term.

The questions we get asked most often

Self-employed clients tend to come to us with a similar set of questions:

- Is my income too complicated for this kind of finance?

- Will lenders want years’ worth of accounts and trading history?

- How do I show I’ve got a credible exit strategy?

- Are the costs going to eat into my profit margins?

- Is this better than going down the traditional mortgage route?

These are all completely fair things to want to understand. Commercial finance isn’t a substitute for standard lending — it’s a specific tool for specific situations, and it’s worth being clear on that distinction before you commit to anything.

Things to think about before you apply

Before you go ahead with either a bridging loan or a development finance facility, it’s worth taking a step back and asking whether it genuinely suits your situation.

The single most important factor is your exit strategy. Lenders will want to see a clear, realistic plan for how the loan gets repaid — whether through a sale, a refinance, or something else. If that isn’t nailed down, it’s going to be a difficult conversation.

Costs need careful thought too. Interest rates, arrangement fees, valuation costs, legal fees — it all adds up, and you need to have done the maths properly before you factor any of this into your projections.

Your experience level matters as well. First-time developers can access funding, but more experienced applicants will generally find a wider range of lenders willing to work with them on better terms.

And finally, the property or development itself — its quality, condition, and location — will all play a significant part in how lenders assess the application.

How to give yourself the best chance

Even with commercial finance, being well-prepared still makes a real difference. Clear financial records — even if they’re not the main thing a lender is focused on — will still add weight to your overall profile.

For development finance, a well-structured project plan backed up by realistic costings and sensible

For bridging, the clarity of your exit strategy is everything. That’s where most of the lender’s attention is going to be, so make sure it’s watertight.

Having the right professionals around you — a good accountant, a solicitor who understands property transactions, and an experienced finance adviser — can also make the application process a lot smoother and more straightforward.

Thinking about taking the next step?

If you’re weighing up a development project, considering an auction purchase, or just need short-term funding and want to understand what’s available to you as a self-employed borrower, it’s well worth having a proper conversation with someone who knows this space.

Feel free to give Active Mortgages a call, drop us a message, or pop over to our profile to arrange a chat. We’ll take a proper look at your plans and give you honest, practical guidance on whether bridging finance or development lending is the right fit for what you’re trying to do.