For the majority of self-employed first-time buyers — particularly those working in construction — the road to owning a home can feel like it’s full of obstacles. It’s something we come across regularly with tradespeople and contractors working across the UK. They’re often earning good money, but they’re worried that being self-employed is going to count against them when it comes to getting a mortgage.

The honest answer is that being self-employed won’t stop you from buying your first home. What it does mean is that lenders look at your application in a different way — and understanding how that works puts you in a much stronger position.

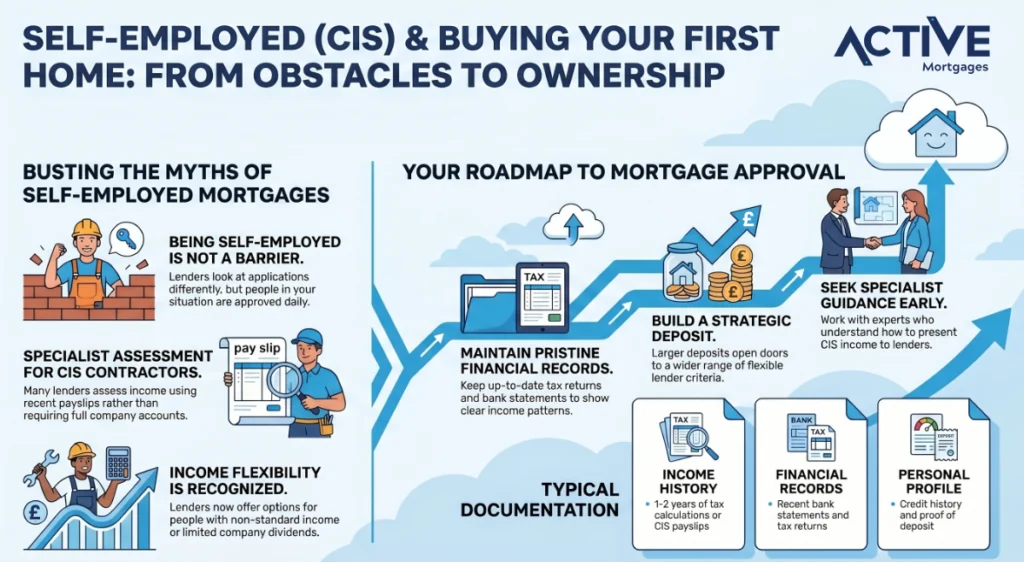

Why self-employed first-time buyers can find it trickier

When you’re employed, lenders can simply look at your payslips and your contract to confirm what you earn. Easy. But for self-employed applicants — especially in construction — income can shift depending on contracts, projects, or the time of year. Even when someone is earning well overall, that variability can make lenders a bit more cautious.

There’s also the question of how you’re actually paid. The majority of people in this situation are paid through a mix of invoices, the Construction Industry Scheme (CIS), or through a limited company. Without proper guidance, it’s easy to get confused about how your income gets calculated and which lenders are even worth approaching.

On top of that, if you’ve moved to the UK from abroad, navigating the mortgage system for the first time — possibly in a second language — adds another layer of complexity that can make the whole thing feel quite daunting.

The good news: people in your situation get approved every day

Despite all of that, self-employed first-time buyers in construction secure mortgages all the time. Lenders have become much more aware of how different industries work, and there are genuinely good options out there for people with non-standard income.

The key is presenting your income clearly and finding lenders whose criteria suit your circumstances. Some lenders, for instance, are perfectly comfortable with CIS contractors and will assess your income based on recent payslips or your contracting history rather than requiring full company accounts.

For limited company directors, some lenders will consider your salary and dividends, while others will also take retained profits into account. Knowing these distinctions can make a real difference to whether your application succeeds.

What lenders are generally looking for

Criteria do vary from lender to lender, but most will want to see:

- A consistent income history. Usually, one to two years of accounts or tax calculations, though some lenders will accept less in the right circumstances.

- Up-to-date financial records. Tax returns, bank statements, and anything else that shows clearly how your income comes in.

- A deposit. First-time buyers who can put down a larger deposit tend to have more options available to them.

- A decent credit history. Lenders will look at your credit profile as part of their overall assessment.

If you’re working under CIS, the requirements can be a bit different, and some lenders offer more flexible assessments based on your recent earnings and work history rather than the standard criteria.

The worries we hear most often

Most self-employed first-time buyers who come to us have a similar list of concerns:

- They think they need several years of self-employment under their belt before they can even apply

- They worry their income won’t be properly understood or accepted

- They’ve been turned down somewhere else and weren’t given a clear reason why

- They have no idea how much they might be able to borrow

These are all completely understandable concerns — but in most cases, they’re solvable with the right advice and by finding the right lender. There’s no one-size-fits-all approach with self-employed mortgage applications, and a bit of tailoring goes a long way.

How to put yourself in the best possible position

If you’re planning to buy your first home, here are a few things that can genuinely help:

• Keep your financial records tidy and up to date. The clearer your documentation, the easier it is for lenders to assess your income — and the fewer questions they’re likely to ask.

• Work with an accountant who knows what mortgage lenders want to see. It’s not just about filing your taxes correctly; it’s about making sure your accounts are presented in a way that works in your favour.

• Try to keep your income as consistent as possible. Big swings in earnings can raise eyebrows, so if you can show a steady pattern, that helps.

• Build your deposit up gradually. Even a slightly bigger deposit can open more doors.

• Keep an eye on your credit file. If there are any issues, it’s much better to deal with them early rather than find out about them halfway through an application.

Specialist support for self-employed construction workers

Active Mortgages specialises in helping self-employed first-time buyers across the UK — including people working in construction under CIS, as sole traders, or through a limited company. We know how these income structures work and, crucially, how to explain them to lenders in a way that makes sense.

Our founder is also a best-selling Amazon author on self-employed mortgages, which reflects just how deeply we’ve focused on this area. That experience means we can guide clients through what can feel like a complicated process with a lot more clarity — especially when applications look a bit unusual on the surface.

We also work regularly with clients from East European backgrounds who are building strong careers in the UK construction industry and are ready to take that next step onto the property ladder.

Conclusion

If you’re self-employed and thinking about buying your first home, it really is worth having a conversation with someone who understands your situation properly.

Feel free to give us a call, drop us a message, or visit our profile to arrange an initial chat. We’ll take a proper look at your circumstances and give you clear, straightforward advice on what your options look like — so you can move forward knowing exactly where you stand.